What is Corporate Laws (Amendment) Bill, 2026, and how will it impact startups, MSMEs, and corporate compliance in India

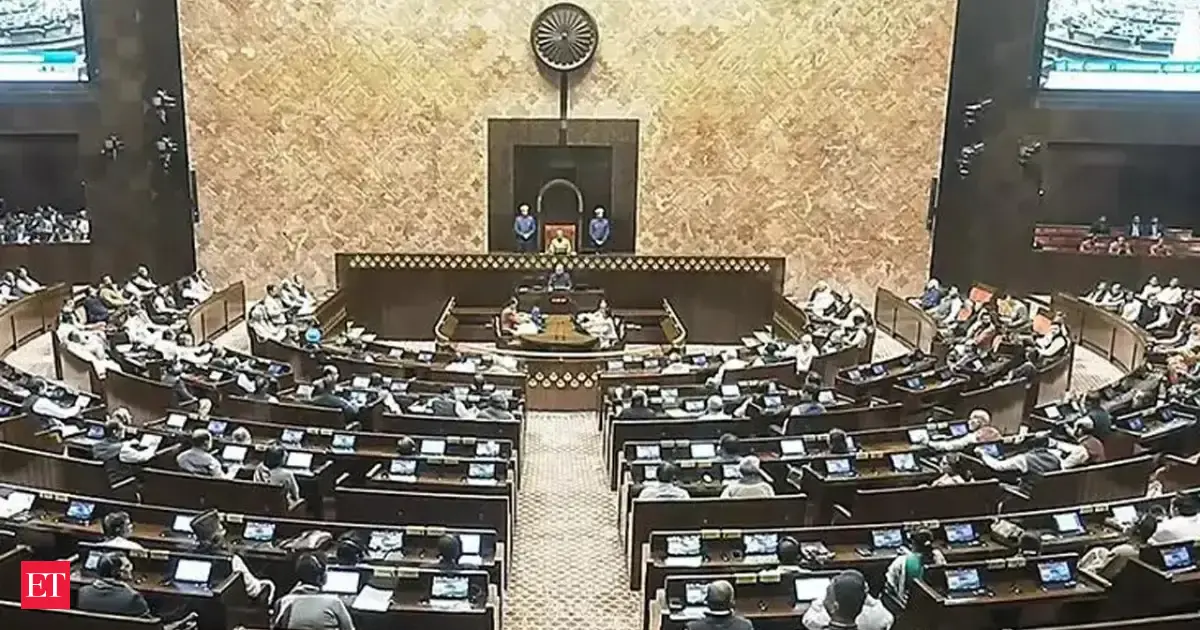

On 23rd March, Finance Minister Nirmala Sitharaman introduced the Corporate Laws (Amendment) Bill, 2026, in the Lok Sabha in a fresh push to simplify business regulations. The House adopted a motion to refer the bill to a Joint Parliamentary Committee (JPC) for detailed examination. The move is part of the government’s ongoing efforts to ease rules governing businesses in India. #BudgetSession2026Finance Minister @nsitharaman introduces The Corporate Laws (Amendment) Bill, 2026 in Lok Sabha. That the Bill further to amend the Limited LiabilityPartnership Act, 2008 and the Companies Act, 2013.@LokSabhaSectt @FinMinIndia @nsitharamanoffc pic.twitter.com/yZKvmfJwNY— SansadTV (@sansad_tv) March 23, 2026 According to the media reports, the bill will focus on making corporate rules more practical and less stressful for businesses, especially startups and small firms. The Union Cabinet had already cleared the bill earlier this month on 10th March, paving the way for its introduction in Parliament. Corporate Laws (Amendment) Bill, 2026 introduced in Lok Sabha, sent to JPChttps://t.co/Gb82rtT0ul— Economic Times (@EconomicTimes) March 23, 2026 Changes to the Companies Act and LLP Framework The new bill proposes amendments to two key laws that govern businesses in India, the Companies Act, 2013 and the Limited Liability Partnership Act, 2008. The Companies Act outlines how companies should be formed, run, and closed. The Limited Liability Partnership Act allows businesses to incorporate a new kind of company in which partners have limited liability. By updating these laws, the government wants to make business operations smoother and reduce unnecessary legal complications. The focus is clearly on making India more business-friendly while also ensuring basic transparency and accountability. Focus on ease of doing business One of the biggest highlights of this bill is that there are plans to decriminalise several minor offences. This means that instead of companies being penalised criminally for minor offences such as procedural errors, they will only have to pay a fine. This will help to reduce the legal risks for entrepreneurs who will be encouraged to do business without fear of severe punishment for minor offences. The bill will “propose several changes for ease of compliance, including decriminalisation of several provisions, regulatory ease for small firms, startups, and producer companies.” Producer companies are companies that are formed by farmers and people who are engaged in agricultural, fishing, and related industries. These companies are expected to benefit from this bill. The bill will also try to simplify the compliance process. This could mean that there will be fewer forms to fill out, fewer procedures to be followed for routine processes such as annual compliance, or other such changes. This will help to reduce the amount of paperwork that companies have to go through and make the system more efficient. Based on expert recommendations The proposed changes are largely based on suggestions made by the Company Law Committee (CLC), which was set up by the government to review corporate laws. The committee, formed in 2019, included experts from different fields such as banking, law, and industry. The CLC had recommended several practical changes, such as allowing companies to communicate with shareholders electronically, making it easier for struggling companies to raise funds, and permitting general meetings in virtual or hybrid formats. It also suggested strengthening regulatory bodies like the National Financial Reporting Authority (NFRA). For LLPs, the committee focused on easing rules for small producer organisations, including those run by farmers, fishermen, and artisans. These recommendations were later reviewed by a high-level panel on regulatory reforms, chaired by Rajiv Gauba. In her earlier budget speech, Sitharaman had said the goal was to “strengthen trust-based economic governance” and improve ease of doing business by reducing excessive inspections and compliance requirements. Link with wider economic reforms The bill also forms a part of a larger effort to improve the business environment of India. At the same time, the government has also initiated several changes to the Insolvency and Bankruptcy Code with a Parliamentary Committee chaired by Bharatiya Janata Party MP Baijayant Panda. Some of the latest recommendations made regarding the bill include: • Stricter timelines for resolving cases of bankruptcy • More power for lenders through the Committee of Creditors (CoC) • The introduction of a system of cross-border insolvency, which will help companies with international operations Proposed changes to CSR rules The government has also planned several important changes to the way Corporate Social Responsibility (CSR) works, which will come through changes made to the Companies Act. One of the biggest changes th

On 23rd March, Finance Minister Nirmala Sitharaman introduced the Corporate Laws (Amendment) Bill, 2026, in the Lok Sabha in a fresh push to simplify business regulations. The House adopted a motion to refer the bill to a Joint Parliamentary Committee (JPC) for detailed examination. The move is part of the government’s ongoing efforts to ease rules governing businesses in India.

#BudgetSession2026Finance Minister @nsitharaman introduces The Corporate Laws (Amendment) Bill, 2026 in Lok Sabha. That the Bill further to amend the Limited LiabilityPartnership Act, 2008 and the Companies Act, 2013.@LokSabhaSectt @FinMinIndia @nsitharamanoffc pic.twitter.com/yZKvmfJwNY— SansadTV (@sansad_tv) March 23, 2026

According to the media reports, the bill will focus on making corporate rules more practical and less stressful for businesses, especially startups and small firms. The Union Cabinet had already cleared the bill earlier this month on 10th March, paving the way for its introduction in Parliament.

Corporate Laws (Amendment) Bill, 2026 introduced in Lok Sabha, sent to JPChttps://t.co/Gb82rtT0ul— Economic Times (@EconomicTimes) March 23, 2026

Changes to the Companies Act and LLP Framework

The new bill proposes amendments to two key laws that govern businesses in India, the Companies Act, 2013 and the Limited Liability Partnership Act, 2008. The Companies Act outlines how companies should be formed, run, and closed. The Limited Liability Partnership Act allows businesses to incorporate a new kind of company in which partners have limited liability.

By updating these laws, the government wants to make business operations smoother and reduce unnecessary legal complications. The focus is clearly on making India more business-friendly while also ensuring basic transparency and accountability.

Focus on ease of doing business

One of the biggest highlights of this bill is that there are plans to decriminalise several minor offences. This means that instead of companies being penalised criminally for minor offences such as procedural errors, they will only have to pay a fine. This will help to reduce the legal risks for entrepreneurs who will be encouraged to do business without fear of severe punishment for minor offences.

The bill will “propose several changes for ease of compliance, including decriminalisation of several provisions, regulatory ease for small firms, startups, and producer companies.” Producer companies are companies that are formed by farmers and people who are engaged in agricultural, fishing, and related industries. These companies are expected to benefit from this bill.

The bill will also try to simplify the compliance process. This could mean that there will be fewer forms to fill out, fewer procedures to be followed for routine processes such as annual compliance, or other such changes. This will help to reduce the amount of paperwork that companies have to go through and make the system more efficient.

Based on expert recommendations

The proposed changes are largely based on suggestions made by the Company Law Committee (CLC), which was set up by the government to review corporate laws. The committee, formed in 2019, included experts from different fields such as banking, law, and industry.

The CLC had recommended several practical changes, such as allowing companies to communicate with shareholders electronically, making it easier for struggling companies to raise funds, and permitting general meetings in virtual or hybrid formats. It also suggested strengthening regulatory bodies like the National Financial Reporting Authority (NFRA).

For LLPs, the committee focused on easing rules for small producer organisations, including those run by farmers, fishermen, and artisans.

These recommendations were later reviewed by a high-level panel on regulatory reforms, chaired by Rajiv Gauba. In her earlier budget speech, Sitharaman had said the goal was to “strengthen trust-based economic governance” and improve ease of doing business by reducing excessive inspections and compliance requirements.

Link with wider economic reforms

The bill also forms a part of a larger effort to improve the business environment of India. At the same time, the government has also initiated several changes to the Insolvency and Bankruptcy Code with a Parliamentary Committee chaired by Bharatiya Janata Party MP Baijayant Panda.

Some of the latest recommendations made regarding the bill include:

• Stricter timelines for resolving cases of bankruptcy

• More power for lenders through the Committee of Creditors (CoC)

• The introduction of a system of cross-border insolvency, which will help companies with international operations

Proposed changes to CSR rules

The government has also planned several important changes to the way Corporate Social Responsibility (CSR) works, which will come through changes made to the Companies Act.

One of the biggest changes that has been proposed includes a lowering of the financial threshold for companies that have to spend money on CSR. Currently, companies with a net profit of more than ₹5 crore have to spend at least 2% of their average profits earned over the last three years on corporate social responsibility activities. This amount may now be reduced to ₹3 crore. This means many more mid-sized companies will now come under the CSR rules for the first time.

Another key change is related to how CSR committees are formed within companies. The proposal says that at least one member of the committee should have proper experience in planning and handling CSR projects. This is being done to make sure that CSR work is taken seriously and not treated as just a formality.

Understanding the existing laws

The Companies Act, 2013, is the main law that governs corporate entities in India. It covers everything from company registration and management to financial reporting and closure. Over the years, this law has been amended multiple times, in 2015, 2017, 2019, and 2020, mainly to simplify compliance and reduce penalties.

On the other hand, the Limited Liability Partnership Act, 2008, offers a more flexible business model. Under the act, partners can run a business without being held liable for its losses up to a certain extent. This model has been more popular among small businesses and professional organisations.

Both laws have already seen reforms in the past, but the 2026 bill aims to further update them based on current business needs.

Key benefits of the Corporate Laws 2026

If passed, the Corporate Laws (Amendment) Bill, 2026, could bring real benefits for businesses across the country. Lower compliance costs, fewer legal hurdles, and simpler processes can make it easier for companies to grow and operate smoothly.

The new amendments can prove to be a boon for startups and small businesses, which might help remove the fear of facing penalties. It can also help boost investor sentiment as the new amendments focus on transparency and governance. And for the overall economy, a more business-friendly environment can attract investment and create jobs.

With the current economic conditions being unpredictable globally, the new bill can be a welcome move towards establishing India as a more reliable business destination.